Flexible Financing with Conventional Loans

A great option for buyers with good credit and stable income, conventional loans offer low rates, flexible terms, and competitive down payment options.

A Smart Mortgage Choice for Many Homebuyers.

A conventional loan is a mortgage that is not backed by the federal government, making it a great choice for borrowers with good credit and stable income. These loans are offered by private lenders and follow guidelines set by Fannie Mae and Freddie Mac.

Key Benefits of Conventional Loans:

Competitive Interest Rates – Lower rates for qualified borrowers.

Flexible Loan Terms – Choose between 10, 15, 20, or 30-year loan options.

Low Down Payment Options – As little as 3% down for eligible buyers.

No Upfront Mortgage Insurance – Unlike FHA loans, PMI can be removed once 20% equity is reached.

More Property Options – Can be used for primary homes, vacation homes, and investment properties

Who Qualifies for a Conventional Loan?

To be eligible for a conventional mortgage, borrowers typically need to meet the following criteria:

Credit Score: 620+ (Higher scores qualify for better rates)

Debt-to-Income Ratio (DTI): 43% or lower (Some lenders may allow up to 50%)

Down Payment: As low as 3% for first-time buyers, but 5-20% is recommended to avoid PMI.

Loan Limits: Up to $766,550 in most areas ($1,149,825 in high-cost areas)

Stable Employment & Income: Two years of steady income history preferred

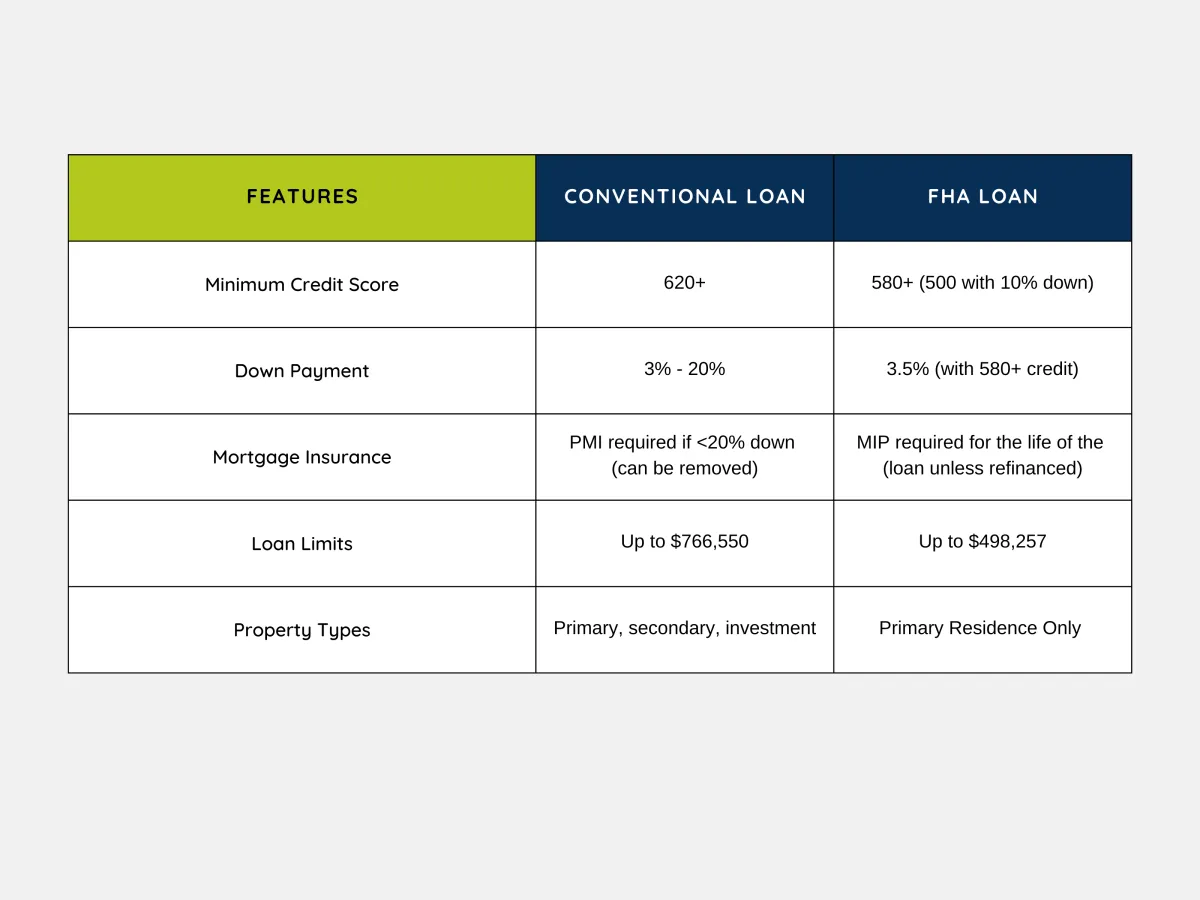

Conventional vs. FHA Loans – A Quick Comparison

Below are the loan programs we offer, each designed to fit different homebuyer needs. Click each option to learn more about eligibility, benefits, and application steps.

Which One is Best for You?

A Conventional Loan is better if you have strong credit and can put at least 3-5% down.

An FHA Loan is better if you have a lower credit score and need a more flexible down payment option.

Conventional vs. FHA Loans – A Quick Comparison

Below are the loan programs we offer, each designed to fit different homebuyer needs. Click each option to learn more about eligibility, benefits, and application steps.

Which One is Best for You?

A Conventional Loan is better if you have strong credit and can put at least 3-5% down.

An FHA Loan is better if you have a lower credit score and need a more flexible down payment option.

Explore Your Conventional Loan Options

Fixed-Rate Conventional Loan

Predictable payments with 10, 15, 20, or 30-year terms.

Best for buyers who want long-term stability.

Adjustable-Rate Mortgage (ARM)

Lower initial interest rates that adjust over time.

Best for buyers planning to sell or refinance within a few years.

Jumbo Conventional Loan

For loans exceeding $766,550 in most areas.

Best for high-value home purchases.

Common Questions About Conventional Loans.

How much do I need for a down payment?

Most conventional loans require 5-20% down, but first-time buyers can qualify for as little as 3% down.

Do I need mortgage insurance?

Private Mortgage Insurance (PMI) is required if you put less than 20% down but can be removed once you reach 20% equity.

Can I use a conventional loan for an investment property?

Yes! Unlike FHA or VA loans, conventional loans allow you to finance vacation homes and rental properties.

What credit score do I need?

A 620+ score is generally required, but higher scores get better interest rates.

Take the First Step Toward Homeownership.

A Conventional Loan offers flexibility, competitive rates, and the ability to avoid mortgage insurance costs over time. Let’s find the best option for you today!

Harmony Home Mortgage provides expert home loan solutions, including FHA, VA, Conventional, USDA, and Non-QM loans. Licensed in FL, GA, NC, SC, and MI, we make homeownership simple and stress-free.

Business Hours

Monday – Friday: 9 AM – 6 PM

Saturday: 10 AM – 2 PM

Sunday: Closed

Mortgage Services

Resources

Company

Legal & Compliance

Harmony Home Mortgage is an independent mortgage broker licensed in Florida, Georgia, North Carolina, and Michigan.

NMLS ID: 1162063

Business NMLS ID: 2629625

All loans are subject to underwriting approval. This is not a commitment to lend. Terms and conditions apply.

Legal Pages

Follow Us Online

Blog Sign Up

Stay updated on mortgage tips, market trends, and homebuying resources.

Harmony Home Mortgage provides expert home loan solutions, including FHA, VA, Conventional, USDA, and Non-QM loans. Licensed in FL, GA, MI, and NC, we make homeownership simple and stress-free.

Business Hours

Monday – Friday: 9 AM – 6 PM

Saturday: 10 AM – 2 PM

Sunday: Closed

Mortgage Services

Resources

Company

Legal & Compliance

Legal & Compliance

Harmony Home Mortgage is an independent mortgage broker licensed in Florida, Georgia, and Michigan.

NMLS ID: 1162063

Business NMLS ID: 2629625

All loans are subject to underwriting approval. This is not a commitment to lend. Terms and conditions apply.

Legal Pages

Follow Us Online

Newsletter Sign Up

Stay updated on mortgage tips, market trends, and homebuying resources.