USDA Loans:

Zero Down Financing for Rural & Suburban Homes

A USDA loan offers 100% financing, low interest rates, and flexible credit requirements, making homeownership more accessible in eligible areas.

USDA Loans:

Zero Down Financing for Rural & Suburban Homes

A USDA loan offers 100% financing, low interest rates, and flexible credit requirements, making homeownership more accessible in eligible areas.

Making Homeownership Affordable with Zero Down.

A USDA loan is a government-backed mortgage provided by the U.S. Department of Agriculture (USDA) to help low- to moderate-income buyers purchase homes in eligible rural and suburban areas.

Key Benefits of USDA Loans:

100% Financing – No down payment required

Lower Interest Rates – Government-backed loans mean competitive rates

Flexible Credit Requirements – Minimum 640+ credit score preferred, but some lenders accept lower scores

Reduced Mortgage Insurance – Lower monthly costs compared to FHA loans

Lenient Income Guidelines – Available to moderate-income households

Who Qualifies for a USDA Loan?

To qualify for a USDA loan, borrowers must meet both property location and financial criteria.

Property Requirements:

Must be in a USDA-eligible rural or suburban area (Check eligibility with the USDA property lookup tool).

Home must be used as a primary residence (No vacation or investment properties).

Must meet USDA property condition requirements (Safe, livable home).

Financial Requirements:

Credit Score: 640+ preferred (some lenders allow lower scores with compensating factors).

Debt-to-Income (DTI) Ratio: Typically 41% or lower.

Household Income Limits: Must be below 115% of the area’s median income (Varies by location).

Stable Employment & Income History: Two years preferred.

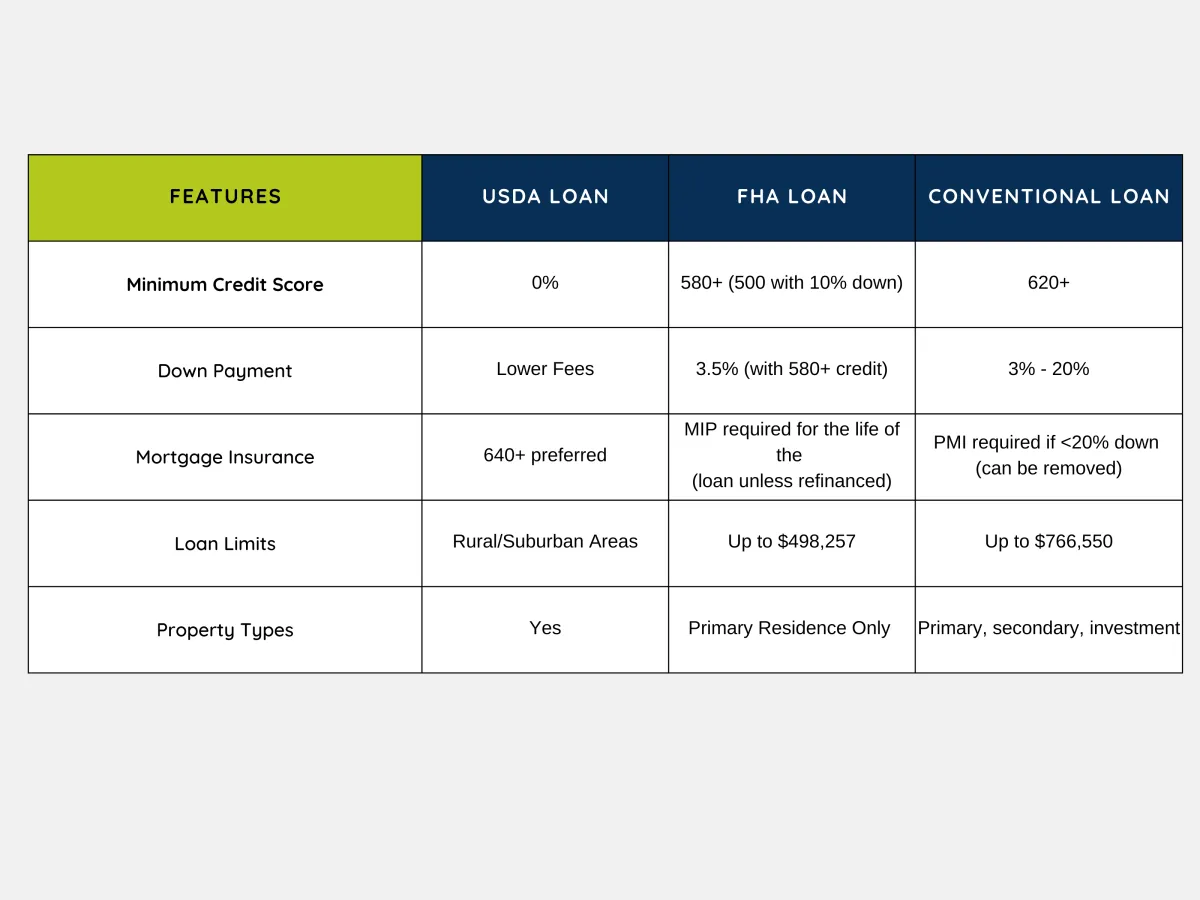

How Does a USDA Loan Compare?

Below are the loan programs we offer, each designed to fit different homebuyer needs. Click each option to learn more about eligibility, benefits, and application steps.

Who Should Choose a USDA Loan?

First-time or repeat buyers looking for zero down payment options.

Borrowers who want lower mortgage insurance costs than FHA loans.

Buyers with moderate income levels in USDA-eligible areas.

How Does a USDA Loan Compare?

Below are the loan programs we offer, each designed to fit different homebuyer needs. Click each option to learn more about eligibility, benefits, and application steps.

Who Should Choose a USDA Loan?

First-time or repeat buyers looking for zero down payment options.

Borrowers who want lower mortgage insurance costs than FHA loans.

Buyers with moderate income levels in USDA-eligible areas.

Explore USDA Loan Options.

USDA Guaranteed Loan (Most Common)

Available through approved lenders with 100% financing.

Designed for low-to-moderate-income buyers.

USDA Direct Loan (For Low-Income Buyers)

Funded directly by the USDA

borrowers who can’t qualify for other mortgages

USDA Streamlined Refinance

Available for current USDA loan holders looking to lower interest rates

Answers to Common USDA Loan Questions

Do I have to be a first-time homebuyer to use a USDA loan?

No, both first-time and repeat buyers can use a USDA loan.

How do I know if a home qualifies for a USDA loan?

You can check the USDA property eligibility map or ask a mortgage expert.

Are there income limits for USDA loans?

Yes, your household income must be below 115% of the area median income.

Do USDA loans require mortgage insurance?

Yes, but the fees are lower than FHA loans.

How long does a USDA loan take to close?

Most USDA loans close within 30-45 days, but processing times can vary.

Answers to Common USDA Loan Questions

Do I have to be a first-time homebuyer to use a USDA loan?

No, both first-time and repeat buyers can use a USDA loan.

How do I know if a home qualifies for a USDA loan?

You can check the USDA property eligibility map or ask a mortgage expert.

Are there income limits for USDA loans?

Yes, your household income must be below 115% of the area median income.

Do USDA loans require mortgage insurance?

Yes, but the fees are lower than FHA loans.

How long does a USDA loan take to close?

Most USDA loans close within 30-45 days, but processing times can vary.

Achieve Homeownership with Zero Down

If you’re looking for affordable homeownership in a rural or suburban area, a USDA loan could be your best option. Let’s get you pre-approved today!

Harmony Home Mortgage provides expert home loan solutions, including FHA, VA, Conventional, USDA, and Non-QM loans. Licensed in FL, GA, NC, SC, and MI, we make homeownership simple and stress-free.

Business Hours

Monday – Friday: 9 AM – 6 PM

Saturday: 10 AM – 2 PM

Sunday: Closed

Mortgage Services

Resources

Company

Legal & Compliance

Harmony Home Mortgage is an independent mortgage broker licensed in Florida, Georgia, North Carolina, and Michigan.

NMLS ID: 1162063

Business NMLS ID: 2629625

All loans are subject to underwriting approval. This is not a commitment to lend. Terms and conditions apply.

Legal Pages

Follow Us Online

Blog Sign Up

Stay updated on mortgage tips, market trends, and homebuying resources.

Harmony Home Mortgage provides expert home loan solutions, including FHA, VA, Conventional, USDA, and Non-QM loans. Licensed in FL, GA, MI, and NC, we make homeownership simple and stress-free.

Business Hours

Monday – Friday: 9 AM – 6 PM

Saturday: 10 AM – 2 PM

Sunday: Closed

Mortgage Services

Resources

Company

Legal & Compliance

Legal & Compliance

Harmony Home Mortgage is an independent mortgage broker licensed in Florida, Georgia, and Michigan.

NMLS ID: 1162063

Business NMLS ID: 2629625

All loans are subject to underwriting approval. This is not a commitment to lend. Terms and conditions apply.

Legal Pages

Follow Us Online

Newsletter Sign Up

Stay updated on mortgage tips, market trends, and homebuying resources.